All inclusive travel groups are so large and ubiquitous it is almost impossible to travel overseas without using one of their airlines, cruiseliners or hotels. Barceló touts 90+ direct companies, Melía has 144 companies and TUI AG has 677 direct and indirect subsidiaries.

From the perspective of the holiday host countries, sun, sand and sea tourism are traditionally considered as a way to generate economic growth. Local government officials tout vacuous GDP growth figures, while hospitality companies make inflated claims of employment, to garner federal funding for infrastructure expansion.

But infrastructure is just one of the motivations for these powerful and vast corporations to invest. Ostensibly, tourist satisfaction drives resort selection. But visibly, much investment is driven by windfall profits and “tax-loss carry-forwards”, thanks to legislated tax loopholes and willing local officials who either ignore or aid in the violation of tax, environmental and employment regulations. (A tax loss carryforward is a loss on operations in the current year that can be carried forward to future years’ profits to be deducted against those gains.)

When the losses are large, accounting rules stipulate that companies can only record on their balance sheets the fraction that is reasonably expected to be recovered or offset – called realizable loss carryforwards. The amounts of loss carry-forwards were so large, that only a portion of them is realisable.

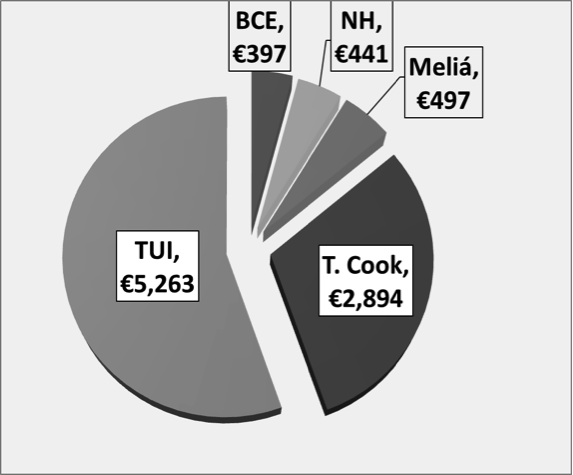

For example, of the €5.3 billion that TUI had accumulated as of 2012, it only expects to deduct €217 m, less than five percent. Thomas Cook will deduct five percent of its losses; Spain’s Barceló 12 percent; Melia 14 percent; and NH 32 percent. These loss carryforwards are so large that even if these webs of companies began paying their fair share today, they would pay no taxes until 2020 and beyond.

While losses are declared at head offices in Spain and Germany, the surplus cash generated by tax credits is then re-invested in new or expanded hotel properties at the same destinations such as Mexico’s Cancún and Riviera Maya as foreign direct investment (FDI) – channeled through tax havens rather than directly from Spain.

More than 80% of the hotel rooms in the Mexican Caribbean are All-Inclusive and 80% of the owners of these are Spanish groups. Yet the FDI patterns don’t reflect this at all: investment levels from Spain are the same as the national average for all of Mexico for all types of investment – while the countries with above-average investment levels were Panama, Switzerland, the Netherlands and the British Virgin Islands: all well-known tax havens.

Thanks to their tax schemes, only an estimated 20% of the package price arrives at the destination, which deprives the host destinations of resources to ensure sustainability.

- Read the original article: Guest blog: sun, sea, sand, tourism and fantasy finance

- Listen to the author interviewed in this podcast

- Or download chapters from or buy the book: Ambrosie, L. M. (2015). Sun & Sea Tourism: Fantasy and Finance of the All-Inclusive Industry. Cambridge, UK: Cambridge Scholars Publishing http://www.tourismfantasyandfinance.org/

{kind=link}

{kind=link}